任务目标

- 实战:python爬取金融数据

- 实战2: 利用python进行金融数据处理:数据清洗,数据可视化,特征提取,etc.

- 实战3:你的第一个基于机器学习的量化模型(yay)

1 数据

金融数据源

存储方式:csv、sql、nosql

数据格式

- 交易所信息

- 数据来源

- Ticker/symbol

- 价格

- 企业行为(stock splits/dividend adjustments)

- 国家假日

数据的注意点

- 企业行为

- 数据峰值

- 数据缺失

2 MySQL

四个基本表:

- Exchange 交易所基本信息表

CREATE TABLE `exchange` (

id int NOT NULL AUTO_INCREMENT,

abbrev varchar(32) NOT NULL,

name varchar(255) NOT NULL,

city varchar(255) NULL,

country varchar(255) NULL,

currency varchar(64) NULL,

timezone_offset time NULL,

created_date datetime NOT NULL,

last_updated_date datetime NOT NULL,

PRIMARY KEY (id)

) ENGINE=InnoDB AUTO_INCREMENT=1 DEFAULT CHARSET=utf8;

- DataVendor 数据来源表 ```sql CREATE TABLE `data_vendor` (

id int NOT NULL AUTO_INCREMENT,

name varchar(64) NOT NULL,

website_url varchar(255) NULL,

support_email varchar(255) NULL,

created_date datetime NOT NULL,

last_updated_date datetime NOT NULL,

PRIMARY KEY (id)

) ENGINE=InnoDB AUTO_INCREMENT=1 DEFAULT CHARSET=utf8;

- Symbol 股票代码与基本信息 ```SQL CREATE TABLE `symbol` (

id int NOT NULL AUTO_INCREMENT,

exchange_id int NULL,

ticker varchar(32) NOT NULL,

instrument varchar(64) NOT NULL,

name varchar(255) NULL,

sector varchar(255) NULL,

currency varchar(32) NULL,

created_date datetime NOT NULL,

last_updated_date datetime NOT NULL,

PRIMARY KEY (id),

KEY index_exchange_id (exchange_id)

) ENGINE=InnoDB AUTO_INCREMENT=1 DEFAULT CHARSET=utf8;

- DailyPrice 每日价格表 ```sql CREATE TABLE `daily_price` (

id int NOT NULL AUTO_INCREMENT,

data_vendor_id int NOT NULL,

symbol_id int NOT NULL,

price_date datetime NOT NULL,

created_date datetime NOT NULL,

last_updated_date datetime NOT NULL,

open_price decimal(19,4) NULL,

high_price decimal(19,4) NULL,

low_price decimal(19,4) NULL,

close_price decimal(19,4) NULL,

adj_close_price decimal(19,4) NULL,

volume bigint NULL,

PRIMARY KEY (id),

KEY index_data_vendor_id (data_vendor_id),

KEY index_symbol_id (symbol_id)

) ENGINE=InnoDB AUTO_INCREMENT=1 DEFAULT CHARSET=utf8;

打通MySQL和python:

sudo apt-get install libmysqlclient-dev pip install mysqlclient

3 数据爬取

3.1 代码解析

- 前往wiki页面获取标普500的企业列表(

obtain_parse_wiki_snp500),并存储到mysql(insert_snp500_symbols)。

def obtain_parse_wiki_snp500():

# Download and parse the Wikipedia list of S&P500

# constituents using requests and BeautifulSoup.

# Returns a list of tuples for to add to MySQL.

# Stores the current time, for the created_at record

now = datetime.datetime.utcnow()

# Use requests and BeautifulSoup to download the

# list of S&P500 companies and obtain the symbol table

response = requests.get(

"http://en.wikipedia.org/wiki/List_of_S%26P_500_companies"

)

soup = bs4.BeautifulSoup(response.text)

# This selects the first table, using CSS Selector syntax

# and then ignores the header row ([1:])

symbolslist = soup.select('table')[0].select('tr')[1:]

# Obtain the symbol information for each

# row in the S&P500 constituent table

symbols = []

for i, symbol in enumerate(symbolslist):

tds = symbol.select('td')

symbols.append(

(

tds[0].select('a')[0].text, # Ticker

'stock',

tds[1].select('a')[0].text, # Name

tds[3].text, # Sector

'USD', now, now

)

)

return symbols

def insert_snp500_symbols(symbols):

"""

Insert the S&P500 symbols into the MySQL database.

"""

# Connect to the MySQL instance

db_host = 'localhost'

db_user = 'sec_user'

db_pass = 'password'

db_name = 'securities_master'

con = mdb.connect(

host=db_host, user=db_user, passwd=db_pass, db=db_name

)

# Create the insert strings

column_str = """ticker, instrument, name, sector,

currency, created_date, last_updated_date

"""

insert_str = ("%s, " * 7)[:-2]

final_str = "INSERT INTO symbol (%s) VALUES (%s)" % \

(column_str, insert_str)

# Using the MySQL connection, carry out

# an INSERT INTO for every symbol

with con:

cur = con.cursor()

cur.executemany(final_str, symbols)

- 根据读取得到的企业列表(

obtain_list_of_db_tickers),逐一前往爬取雅虎金融抓取每日数据(get_daily_historic_data_yahoo),并存储到MySQL中(insert_daily_data_into_db)。

def obtain_list_of_db_tickers():

"""

Obtains a list of the ticker symbols in the database.

"""

with con:

cur = con.cursor()

cur.execute("SELECT id, ticker FROM symbol")

data = cur.fetchall()

return [(d[0], d[1]) for d in data]

def get_daily_historic_data_yahoo(

ticker, start_date=(2000,1,1),

end_date=datetime.date.today().timetuple()[0:3]

):

"""

Obtains data from Yahoo Finance returns and a list of tuples.

ticker: Yahoo Finance ticker symbol, e.g. "GOOG" for Google, Inc.

start_date: Start date in (YYYY, M, D) format

end_date: End date in (YYYY, M, D) format

"""

# Construct the Yahoo URL with the correct integer query parameters

# for start and end dates. Note that some parameters are zero-based!

ticker_tup = (

ticker, start_date[1]-1, start_date[2],

start_date[0], end_date[1]-1, end_date[2],

end_date[0]

)

yahoo_url = "http://ichart.finance.yahoo.com/table.csv"

yahoo_url += "?s=%s&a=%s&b=%s&c=%s&d=%s&e=%s&f=%s"

yahoo_url = yahoo_url % ticker_tup

# Try connecting to Yahoo Finance and obtaining the data

# On failure, print an error message.

try:

yf_data = requests.get(yahoo_url).text.split("\n")[1:-1]

prices = []

for y in yf_data:

p = y.strip().split(',')

prices.append(

(datetime.datetime.strptime(p[0], '%Y-%m-%d'),

p[1], p[2], p[3], p[4], p[5], p[6])

)

except Exception as e:

print("Could not download Yahoo data: %s" % e)

return prices

def insert_daily_data_into_db(

data_vendor_id, symbol_id, daily_data

):

"""

Takes a list of tuples of daily data and adds it to the

MySQL database. Appends the vendor ID and symbol ID to the data.

daily_data: List of tuples of the OHLC data (with

adj_close and volume)

"""

# Create the time now

now = datetime.datetime.utcnow()

# Amend the data to include the vendor ID and symbol ID

daily_data = [

(data_vendor_id, symbol_id, d[0], now, now,

d[1], d[2], d[3], d[4], d[5], d[6])

for d in daily_data

]

# Create the insert strings

column_str = """data_vendor_id, symbol_id, price_date, created_date,

last_updated_date, open_price, high_price, low_price,

close_price, volume, adj_close_price"""

insert_str = ("%s, " * 11)[:-2]

final_str = "INSERT INTO daily_price (%s) VALUES (%s)" % \

(column_str, insert_str)

# Using the MySQL connection, carry out an INSERT INTO for every symbol

with con:

cur = con.cursor()

cur.executemany(final_str, daily_data)

3.2 其他注意点

pandas直接读取网页

- 有更丰富的宏微观数据

- 注册可以获取更多的api调用次数

- 相关代码可以查看第三课时对应的

quandl_data.py文件

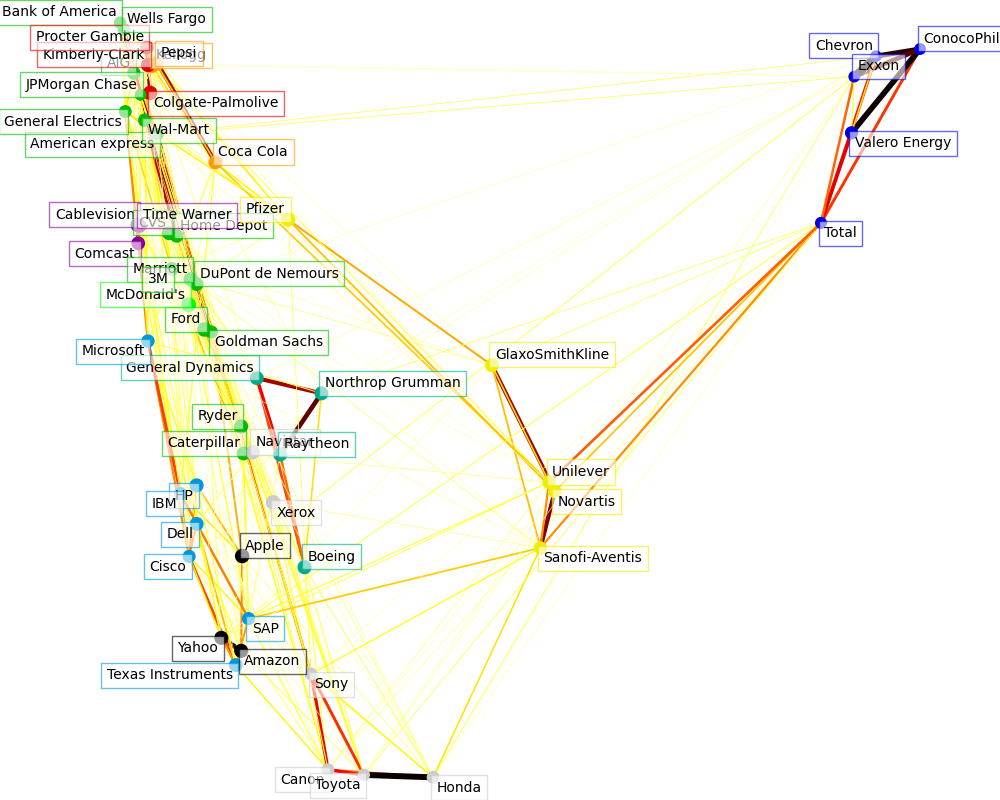

4 案例:沪深300聚类与降维可视化

Visualizing the stock market structure — scikit-learn 0.24.2 documentation

主要流程

- 读取存储在github上的示例数据,并计算开盘价与收盘价的差值

- 对数据进行标准化,并进行基于LARS(最小角回归)的Lasso回归建模

- 对结果通过1_study/algorithm/数据降维算法/局部线性嵌入 LLE进行算法降维

- 将降维后的数据以及聚类结果进行绘图展示

5 时间序列分析

OU(Ornstein-Uhlenbeck)过程(又被称为奥恩斯坦-乌伦贝克过程)

检验时间序列平稳性的常见两种方法,ADF Test 和 Hurst Exponent

平稳性检验方法实战:

- ADF检验直接采用statsmodels库中的现有函数来实现

import statsmodels.tsa.stattools as ts # Calculate and output the CADF test on the residuals cadf = ts.adfuller(df["res"])

- 赫斯特指数的计算比较简单,基础函数就能搞定

from numpy import cumsum, log, polyfit, sqrt, std, subtract from numpy.random import randn def hurst(ts): """Returns the Hurst Exponent of the time series vector ts""" # Create the range of lag values lags = range(2, 100) # Calculate the array of the variances of the lagged differences tau = [sqrt(std(subtract(ts[lag:], ts[:-lag]))) for lag in lags] # Use a linear fit to estimate the Hurst Exponent poly = polyfit(log(lags), log(tau), 1) # Return the Hurst exponent from the polyfit output return poly[0]*2.0